Enabling the mass adoption of in-car commerce - Four times as many drivers now trust OEMs to manage payments following the pandemic.

Parkopedia is scheduled to host a thought-provoking panel talk at CES 2024 on the key role driver trust plays in the growing adoption of in-car commerce. While paying for parking previously involved feeding coins into a parking meter, drivers now have many more ways to pay - from contactless payments to in-car payments. According to Parkopedia’s 2023 Global Driver Survey, it was highlighted that in the last four years, drivers’ acceptance of car manufacturers to manage these payments has tripled globally and quadrupled in the US. Parkopedia’s COO, Hans Puvogel, highlights the significance of this increased trust with OEMs as part of the growth of in-car commerce.

Cars have gone from being a significant ‘one-off’ sale for manufacturers - with the prospect of follow-up servicing income and potential future repeat sales - to a combination of finance monthly payments and recurring payments for an increasing number of connected car services. Executed well, this setup can make drivers’ lives easier and simplify their budgeting, providing them with a broad range of value-added services for an affordable cost and ensuring purchases remain within the OEM’s ecosystem, offering scope for increased brand loyalty.

Insights on the in-car commerce industry

With the insights and data around us, all roads lead to in-car commerce. However, like many connected services, it is not as simple as ‘switching this on’, and some OEMs will be more successful than others in offering and growing these services. I wanted to cover the learnings we have gone through after spending a decade involved with in-car commerce and how OEMs can get ahead of the curve and avoid the pitfalls.

Parking payments: driver trust in car manufacturers quadruples

Back in 2019, only 12% of drivers trusted their car manufacturer to handle payments for parking, with automakers ranking seventh alongside municipalities and only ahead of the ‘other’ category.

Today, car manufacturers have leapt to joint third position globally in the 2023 survey, being trusted by 35% of respondents - just behind specialist parking apps, the second most trusted organisation type, at 36% (with trust in OEMs reaching 37% if figures for Japan and Italy figures were omitted for a like-for-like comparison to 2019). Trust levels have risen most in the US though, quadrupling from 11% to 43% to reach the top position, with a greater proportion of drivers now trusting manufacturers over parking operators.

This 35% figure represents a 23 percentage point increase - a significantly greater rise than any other category recorded, with parking operators scoring the second largest increase at a much lower 7 percentage points. Trust in credit card companies, meanwhile, increased further by 4 percentage points, moving up to a rating of 45% but with the gap closing behind them.

The category that recorded the greatest drop, however, is ‘None, I want to do this myself’, which saw a fall from 19% of drivers not trusting any organisation to manage payments for them in 2019 to just 7% in 2023. This highlights that significantly more drivers are open to trusting external companies to manage parking payments in 2023 than in 2019. Discounting the ‘None’ category, average trust globally has increased from 24.8% to 27.3%, showing that drivers are increasingly more confident in using newer payment methods.

Driver demand for automatic parking payment and navigation soars

Interest amongst motorists for automatic guidance to locations with likely parking/charging availability and personalised parking/charging recommendations remain popular from 2019 to 2023, recording interest levels of over 50% in both surveys. However, demand for automatic payment for on-street parking has nearly doubled in this period, from 23% to 45%.

Similarly, automatic guidance to parking locations closest to the destination has seen a spike in interest with 55% requesting this in 2023, up from 42% in 2019. Interest in being able to automatically open car park barriers and receive monthly invoicing for frictionless access and exit has also nearly doubled, up from 13% to 25%, showing that drivers have a keen interest in being able to simplify the parking, charging and payment process.

The opportunity

Why the car is the next commerce platform

With drivers’ lives becoming increasingly connected across more and more digital devices, driver expectations from their vehicles - typically the most expensive digital device they ever purchase - are growing exponentially. While in-car media used to consist of nothing more than analogue radio, in-car digital technology now includes connected infotainment systems and a host of automated driving systems designed to elevate the driving experience.

Additionally, the growth of in-car services and motorists’ increasing acceptance of subscription models, gives drivers the choice to purchase a range of useful services and enables OEMs and suppliers to offer a broad variety of functions and services as part of a new additional revenue stream.

The expectation that vehicles will become the next commerce platform is based on the inevitable convergence of technological advancements, changes in consumer behaviour, and the desire to leverage the time spent in vehicles for additional services and experiences. As technology continues to advance, vehicles will play an increasingly prominent role as a commerce platform across various domains.

Seamless in-car services boost OEM customer retention

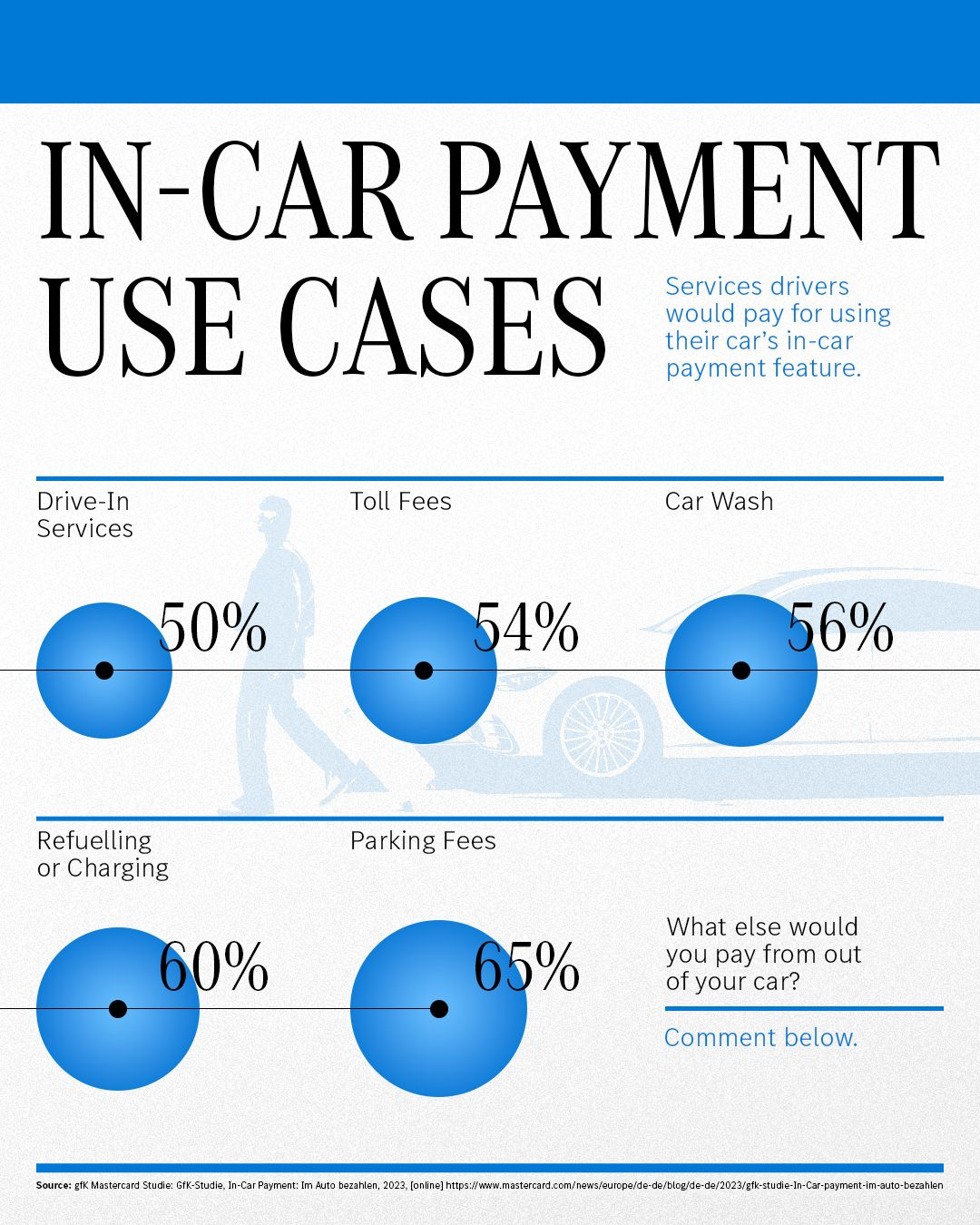

The data shows that drivers highly value well-presented and seamlessly integrated connected car services and are even willing to pay for them. To showcase this, 51% of the 5,454 respondents to our 2023 Global Driver Survey would be willing to pay a premium of up to 10% to park in their preferred location with 19% open to paying more than 10% extra.

It’s a similar story with charging, with 52% of respondents willing to pay a premium of up to 10% to charge in their preferred location, with 15% willing to pay over 10% extra. More than 95% of respondents to the latest China Driver Survey are willing to pay monthly service fees for in-vehicle parking data, with 40% open to paying 5-10 RMB per month for high-quality data.

However, there is a delicate balance for what can be charged to the driver for services that may eventually become the standard due to growing competition and rising expectations around technology and connected services. Drivers are unanimous in wanting intelligent assistance with locating and paying for vehicle-centric services and for these services to complement the driving experience and be easy to use from behind the wheel.

What is critical to be successful for in-vehicle payments?

Getting the enrolment experience right

At CES we will highlight how integrating in-vehicle payments successfully will improve the customer experience and boost brand loyalty. Drivers expect seamless enrolment and single sign-on across in-car services and getting this right can improve drivers’ view of their vehicle and the manufacturer itself.

Smooth enrolment requires the minimum number of steps possible for the full-service portfolio. This should involve no more than four steps - including acceptance of terms and conditions. Meanwhile, individual transactions should require no more than two steps, with distractions removed for the best user experience and the greatest chance of drivers choosing to utilise the service.

Failing to do so, however, dissuades drivers from trying out such services at all and may negatively affect their view of the entire service and potentially the manufacturer itself - even if they never got past the sign-up stage. OEMs must make clear that drivers are not signing up for what is perceived as costly additional services, but using their vehicles to simplify the process of paying for services they are already using.

Seamless connected car services are a significant opportunity for OEMs to improve drivers’ view of their vehicles and to get them attuned to their interfaces, boosting brand loyalty. One highly effective way to increase take-up of connected car services is nudging and prompting users when services are available in the area, using vehicle sensors to recognise where the car is and showing drivers which services are available. From our experience, users typically need to be reminded to use a new service, until they’ve established a habit, so nudges and prompts at the right time can significantly drive transaction rates in the majority of cases.

Providing maximum convenience

Providing driver-focused and value-added execution for in-car commerce can have a drastic impact on adoption rates and driver sentiment, so this plays a significant part in the overall success of in-vehicle payments for OEMs and service providers alike.

Making in-car commerce convenient is paramount to adoption rates, with the combination of in-car payments and navigation providing an improved user experience over having to use multiple services or platforms to access. Leveraging VoiceUI should help to provide a ‘complete user experience’, making such services even more accessible behind the wheel.

OEMs need to add simple and clear user experiences to access services within their infotainment system. Not only should these services be user-friendly, but the functionality also needs to be communicated effectively to drivers to ensure that they are aware of the full suite of services available to them, getting this wrong only detracts from the value drivers see in their vehicles and reduces any attachment to their vehicles and brands.

Drivers also tend to be cautious about who they share their payment card information with, so OEMs need to provide convincing reasons for users to share these with automakers. Demonstrating to drivers the extra level of convenience by taking the pain out of paying for vehicle-centric services through the car helps OEMs to sign up users for their own services such as Feature on Demand.

Comprehensive service provider onboarding - global coverage of services

Seamless onboarding of service providers is central to the success of in-car commerce. Just as drivers need to be encouraged to sign up for in-car payment services, a sufficient pool of service providers is needed to make sure that the breadth and quality of services provided warrant drivers going to the effort of registering in the first place. Leveraging service providers’ brand recognition is an important part of this, promoting companies' established brand logos to gain the trust of end users and grow usage.

Increasingly, drivers don’t just want individual services, but well-thought-out functions that work in unison and bring together information, navigation and transactions, for instance. Providing a seamless service where drivers can find a suitable parking and/or charging location, navigation, pre-book local amenities and arrange payment in one simple process, ensures a superior user experience than simply providing navigation. However, this requires well-executed in-car features and a broad range of services on a global scale.

-

In summary, it is clear how quickly driver interest in in-car commerce is rising and the opportunities this presents to OEMs and service providers. Convenience, price advantage, peace of mind and reliability are the key elements needed to maximise the number of drivers enrolling for in-car commerce features and the ones that continue to use these in the future.

I am looking forward to taking to the stage at CES with my industry peers to share more of my thoughts on the subject and discuss best practices, successful case studies and what we predict in the years ahead for in-vehicle payments.

Register for our in-car commerce breakfast briefing session and panel discussion at CES 2024 to continue the discussion. See you there!