▶️ Click play above to listen to this Blog Post 🎧

Automakers’ remit has broadened dramatically over the last 20 years from simply producing personal transportation to software-defined vehicles where connectivity and functionality are central selling points for many drivers. The quality of media systems, phone connectivity and value-adding features, such as parking data, EV charging information and in-car payments, are becoming vital to 21st-century drivers, who expect seamless connected experiences.

Cars are also turning into ‘mobile data hubs’, providing greater convenience, safety and entertainment features than ever before. This data doesn’t just enable ‘nice-to-have’ non-essential features however, it plays a central role in providing seamless driving experiences that remove the stress from everyday driving, such as finding parking, paying for tolls and fuelling/charging. Being able to offer a broad range of seamless connected car services will play an increasingly significant role in automakers attracting new customers as drivers demand ever more sophisticated in-car services to ensure journeys are efficient and filled with experiences that ‘delight’ the driver.

What do drivers want most?

Gaining popularity year-on-year, being able to gauge parking space availability near their destination is now the most requested connected car feature by drivers worldwide (via probability of choice), according to the 2022 TechInsights Connected Features Interest Report, highlighting strong demand for this among the 4,990 drivers surveyed across the US, China, Germany, France, UK and Italy.

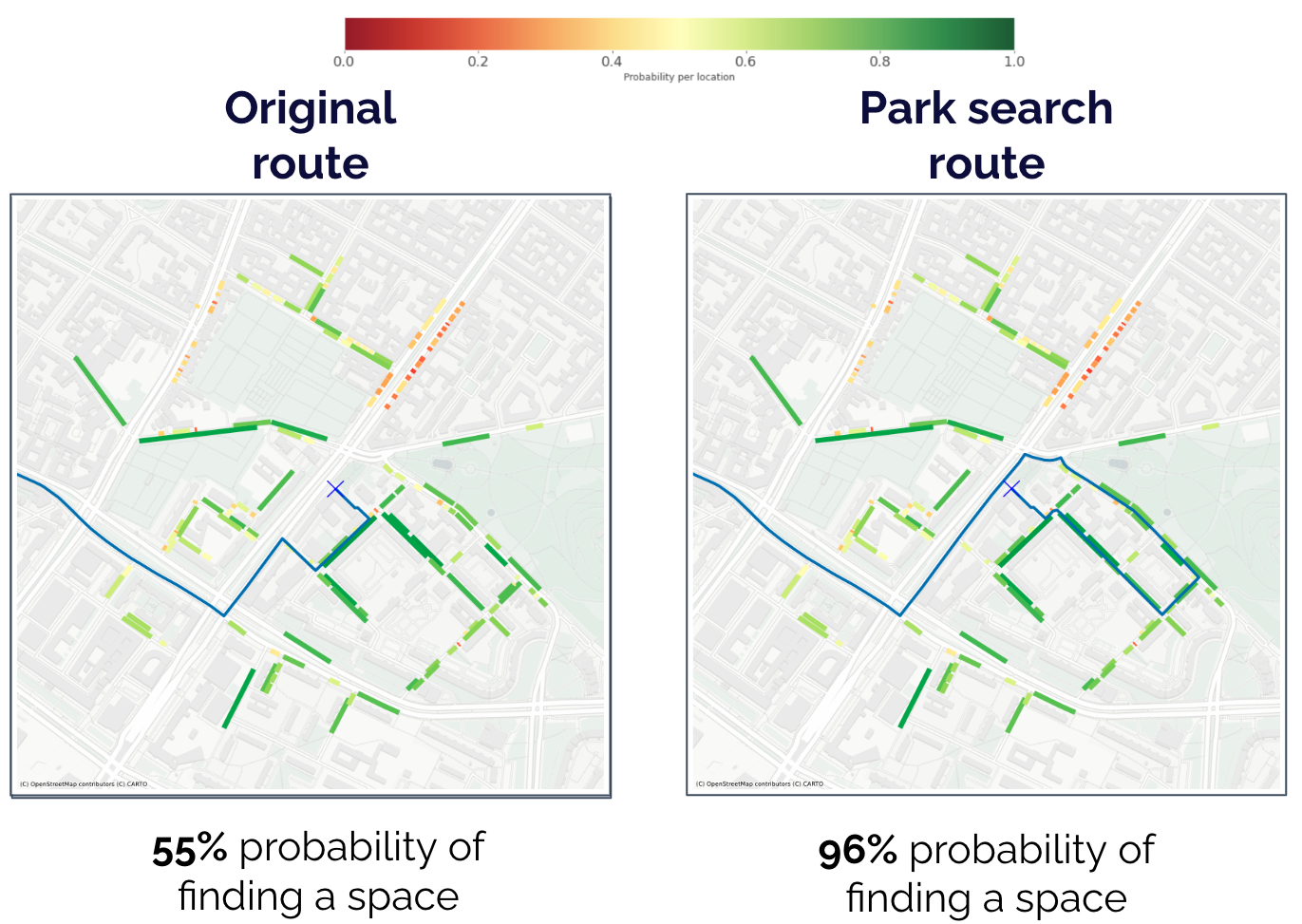

‘Park Search Route’ by Parkopedia drastically improves the probability of finding a parking space near your final destination

Regularly used ‘journey-based’ services such as this are deemed ‘essential features’ by the majority of drivers as part of a convenient driving and navigation experience. However, these desired experiences for navigation, in-car commerce or wider vehicle-centric services, simply aren’t possible without one crucial feature - a base layer of extensive, high-quality accurate data supporting them.

This data is essential for accurately logging location details plus factors such as parking fees, charging costs and any restrictions. Providers such as Google may offer a range of POI data, but this is generally publicly provided, therefore unverified, inaccurate and typically has no dynamic data element to them, making the data outdated almost immediately. This means that companies that rely on this type of ‘off-the-shelf’ data and don’t work with specialist data and connected service companies who verify and validate their data and understand specific drivers’ needs, risk rapidly being left behind competitors in the crucial area of retaining customers with value-added services and successfully monetizing the connected vehicle.

In-Car Commerce

It’s easy to think that all data is equal and can be sourced from any provider, however, transactions - an ever more central part of the SDV strategy - simply will not work without underlying high-quality POI location data. Without highly accurate location information, vehicles are unable to localise and facilitate the correct transaction for parking, charging or other payment services - is the vehicle located in a specific low-cost on-street parking space or a high-cost off-street car park adjacent? Is a car connected to pump four at a fuel station or charger number 2 on the forecourt? What is the likelihood of the charger in question being available at the time of arrival? These distinctions are fundamental to seamless in-car commerce solutions with precise data being a key building block for successful in-car payments.

In-car payments continue to grow in importance to drivers worldwide - across age and technology familiarity levels, according to the TechInsights Connected Features Interest Report. Drivers have greater confidence in these services than in previous years and their expectations are growing too, with more and more motorists wanting their vehicle to manage the payment process for an increasing range of services to assist the convenience factor of their vehicles.

Brand Loyalty via Connected Services

Despite TechInsights data showing that drivers are twice as likely to choose to pay for tolls directly through their vehicle than order food through their car, and around twice as likely to want to pay for parking or fuel than read emails through their car or play online games, some OEMs are still struggling to provide the connected car services that drivers are requesting the most. And those that fail to offer user-friendly in-car services with sufficient features, risk losing a significant proportion of their customers to rival brands as competition has risen significantly from newly established Asian OEMs who already have a strong customer base and a firm grasp on customer loyalty via technology and connected services as part of the ownership experience.

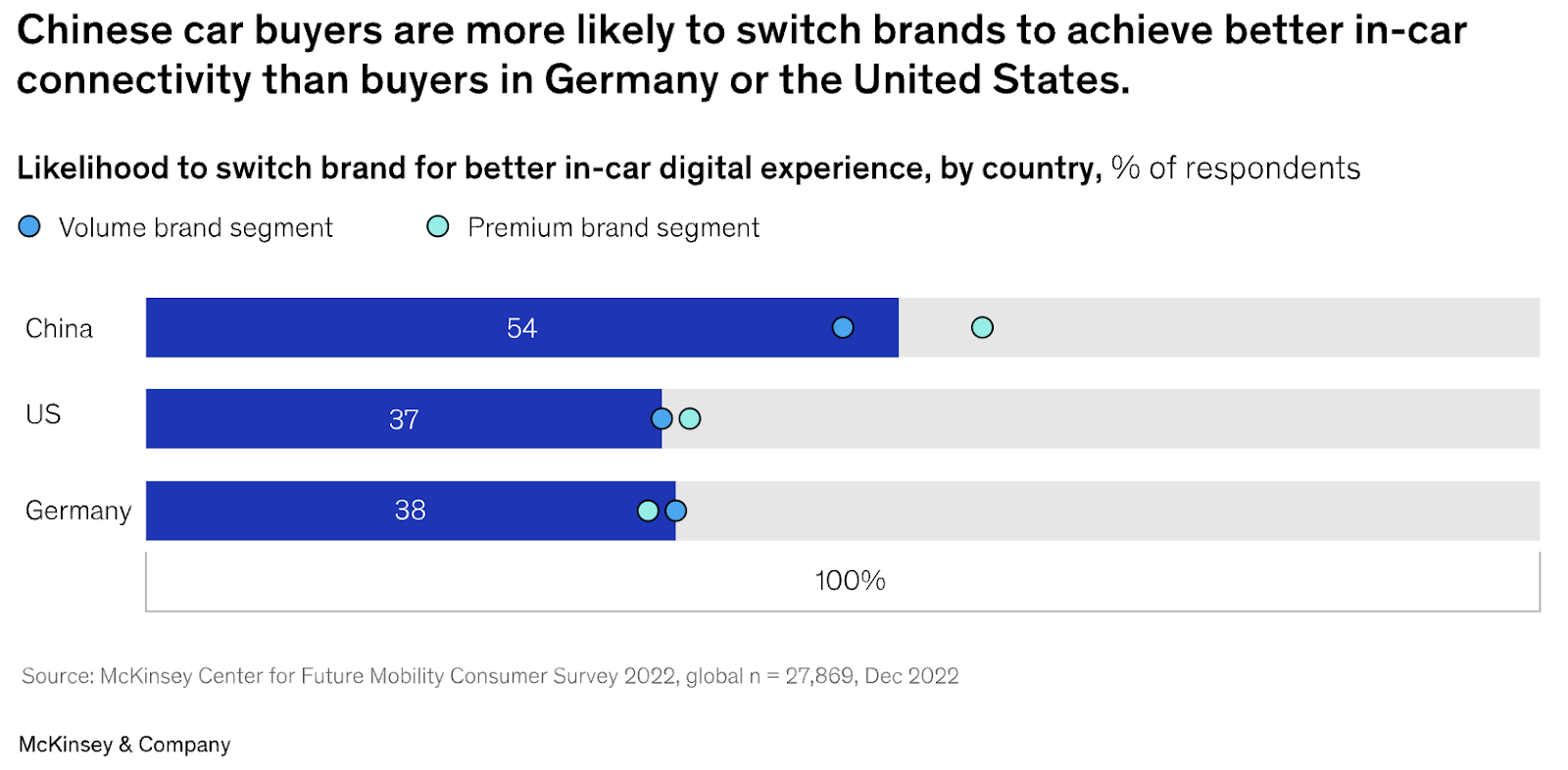

The Chinese car market is the current leader for lacking brand loyalty, with 54% of drivers more likely to switch to a different car brand to gain better in-car connectivity, according to the latest McKinsey Mobility Consumer Pulse Survey. Even in the US and Germany, this figure stands at just below 40% with the gap closing to drivers in China, showing the fundamental role that in-car connected services play in drivers’ choice of vehicle.

Adding to this, only a mere 17% of drivers are satisfied with their current connected services setup, according to a separate report from McKinsey, with features such as in-car payment, intelligent parking spot finders and vehicle Wi-Fi being some of the most valued connected features. This highlights the scale of the risk OEMs expose themselves to by not prioritising connected car services, which is exacerbated by the growing importance of these services to drivers.

Consumers are ‘overwhelmingly satisfied and likely to resubscribe’ when they experience connected car services first-hand, according to a global survey of nearly 8,000 drivers conducted by S&P Global Mobility. 82% of those who had experienced a free trial or had a subscription on a 2016-on car said they would ‘definitely’ or ‘probably’ consider purchasing subscription-based services when they next purchase a car, S&P adds.

As awareness of connected car services improves and drivers expect more and more of these to be integrated into their vehicles, OEMs that fail to provide high-quality services are likely to fall behind. Drivers may not initially notice that valuable services are lacking, however, as with vehicles that offer poor reliability or high running costs, drivers are less likely to buy from the same brand next time around.

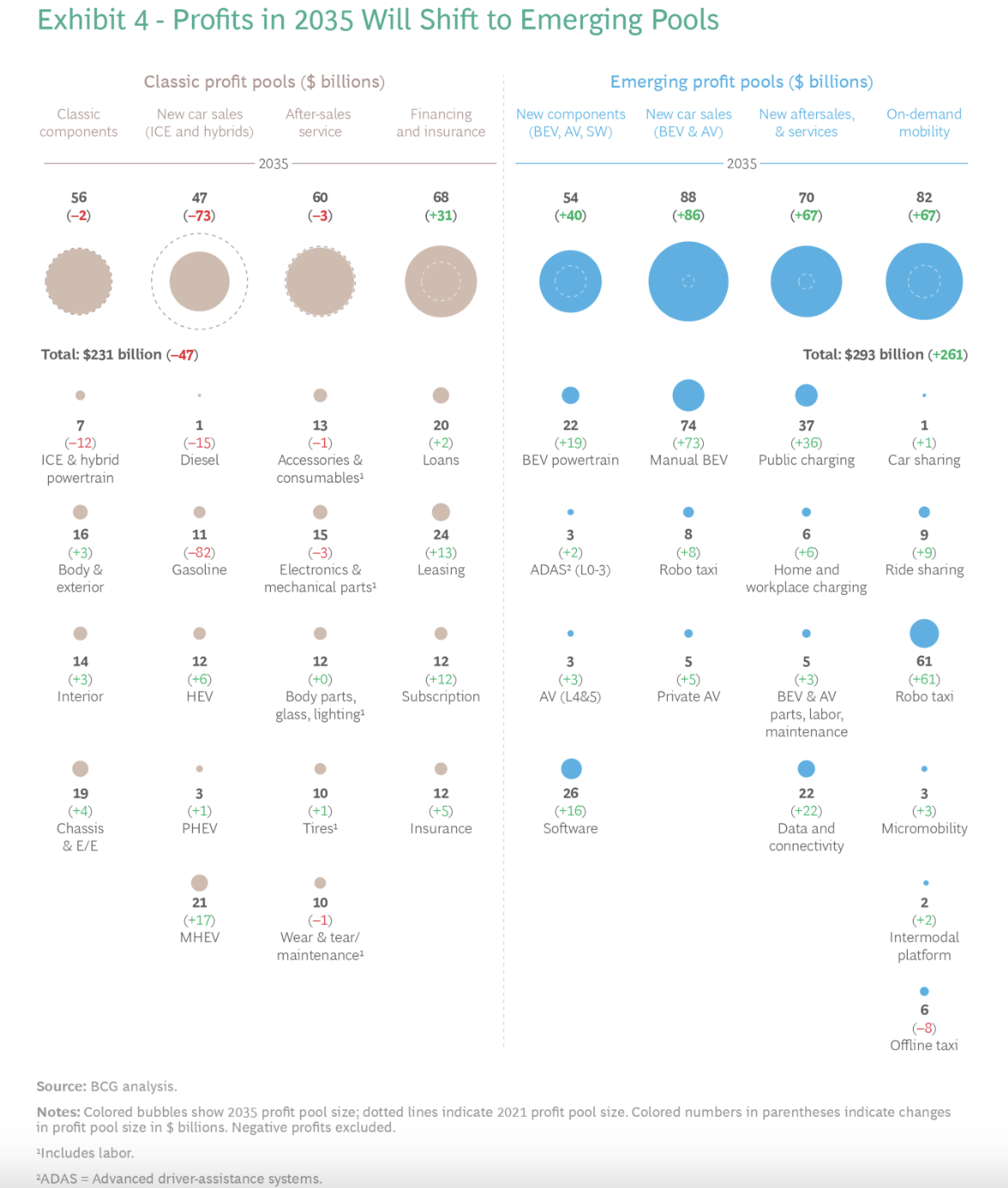

Therefore, connected car services shouldn’t be seen as an expenditure by OEMs but as an investment into potential new revenue streams that provide value to drivers and significantly boost their customer loyalty. Vehicle software profits are expected to reach $49 billion by 2035, according to BCG, with features such as data connectivity services requiring platform-agnostic setups that can be tailored to suit individual manufacturers’ vehicles. Get this right with intelligently set-up data analytics, insights and effective monetisation, and OEMs and drivers stand to benefit greatly.

Many OEMs recognise the potential of in-car payments, but this is a far greater task than simply integrating payment technology into cars. High-quality location data is central to the ability to propose relevant in-car purchases and automakers that realise this and intelligently integrate and combine location technology into their vehicles stand to benefit as the in-car commerce space rapidly expands over the next few years. Brands that are behind the curve, however, may find it difficult to regain lost market share as drivers come to expect the convenience of successful in-vehicle transactions for services that complement the driving experience.